Mortgage Rates and Inflation: What’s Happening Right Now?

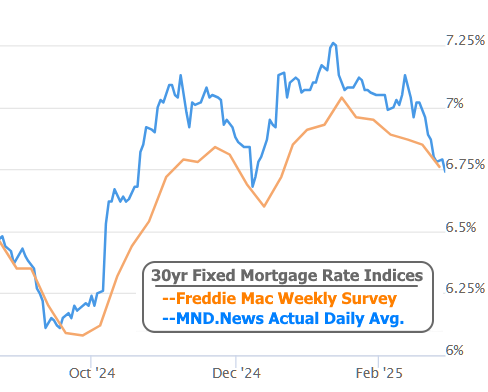

Rates have been consistently moving lower since February 13th and have remained broadly stable since January 15th. There’s a simple reason for this trend—one that’s easier to grasp than you might think.

To explain, let’s first take a quick look at Treasuries, which serve as a benchmark for interest rates like mortgages. The chart below uses “candlesticks,” which show the full day's movement in a single symbol. The bigger the green candle, the better the day was for rates.

As you can see in the chart, January 15th and February 13th kicked off two of the biggest winning streaks for mortgage rates. These dates align with surprisingly low inflation readings. The key takeaway here: rates care a lot about inflation, and when inflation comes in lower than expected, rates tend to drop.

While some might point to February 12th’s inflation data, which came in higher than expected, creating the big red candlestick that day, it’s important to remember that the next day’s data showed the February 12th report was a bit of an outlier. We covered this in more detail in our newsletter at the time.

So, why go into all this detail? Because as of this past Friday, we now have the final word on inflation for January with the release of the PCE Price Index.

PCE is a broader data set compared to the CPI and PPI reports that come out earlier in the month. It was CPI that caused concern on February 12th, while PPI was more of a calming factor. These reports often give us an early preview of what to expect from PCE. With PCE now out, it appears that markets did a great job of anticipating the results.

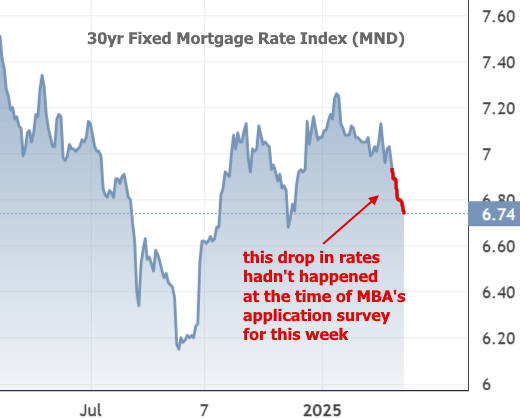

For mortgage rates, this brings the average lender to some of the best levels we've seen since early December—and not far from the best rates since October.

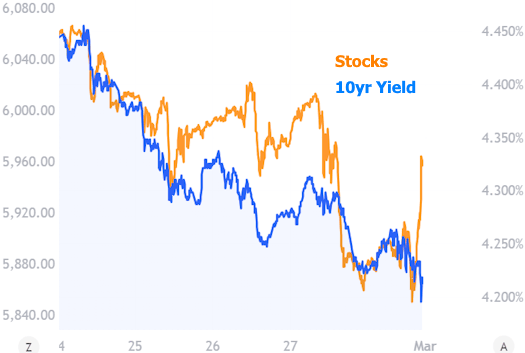

While inflation is the most significant factor affecting rates right now, it's not the only one. Over the past week, we've noticed a stronger correlation between rates and stock prices. However, this is not a long-term trend. Rates can often move opposite of stocks, especially when reacting to Fed policy. For example, the promise of faster rate cuts by the Fed might push stocks higher while rates drop. But when concerns about the economy take center stage, stock prices and rates can move in the same direction.

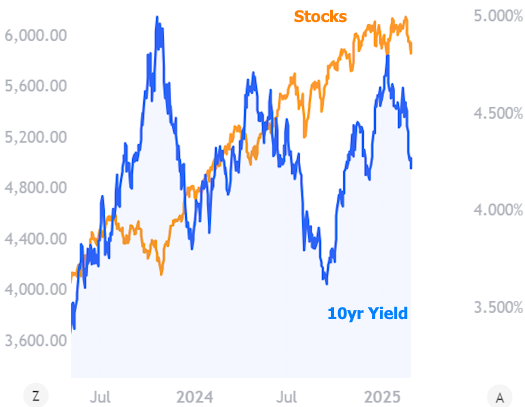

To illustrate how this correlation can be imperfect, consider the same data over a longer time frame:

In terms of other economic data, there wasn’t much this week that significantly impacted rates. However, here’s a quick preview of some notable updates from the mortgage and housing markets:

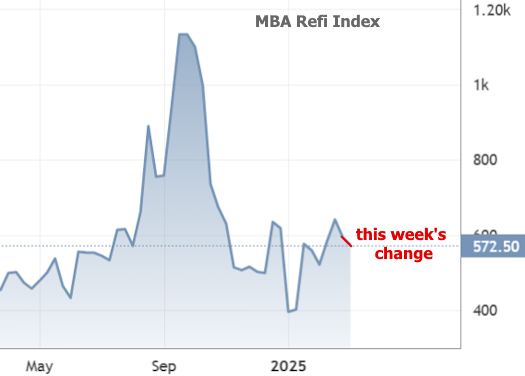

- Mortgage refinance applications decreased slightly according to the MBA. But keep in mind that the recent rate improvements occurred after those survey responses were collected.

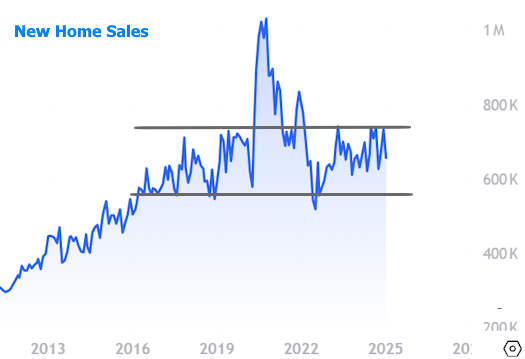

- The Census Bureau reported a 10.5% drop in January’s new home sales. While this may seem like a big decline, the margin of error is large, and the sales pace remains consistent with the trend over the past 8-9 years (excluding the post-COVID spike).

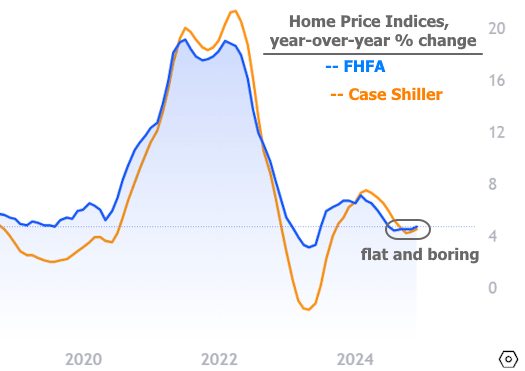

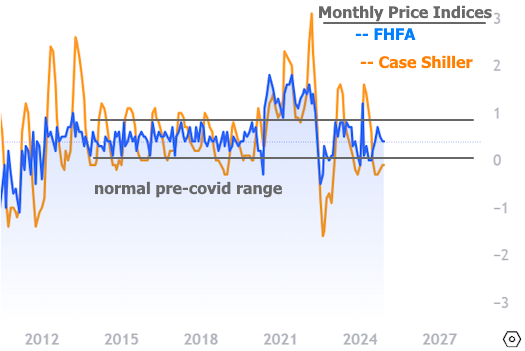

- Home price appreciation is relatively stable, aligning with the levels seen before the pandemic.

Looking ahead, next week brings the most consequential slate of economic data for the month, culminating in the jobs report on Friday. If this report deviates significantly from forecasts, it could have an impact comparable to the inflation reports we’ve been discussing. Other reports throughout the week will also be crucial. If the data points to economic growth or contraction, we can expect mortgage rates to move accordingly (weaker economy = lower rates, stronger economy = higher rates).

Categories

Recent Posts

GET MORE INFORMATION